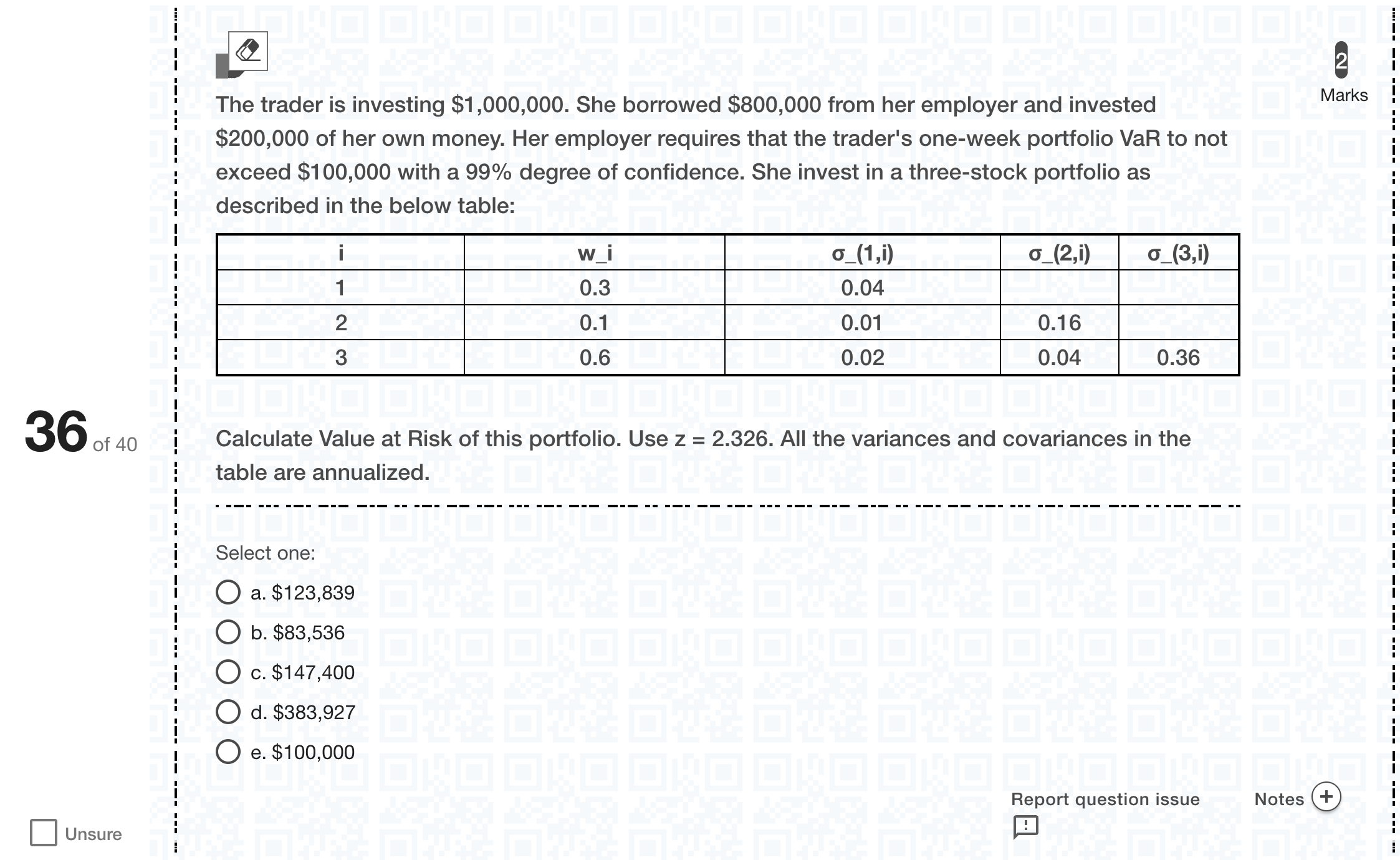

The trader is investing $1,000,000. She borrowed $800,000 from her employer and invested $200,000 of her own money. Her employer requires that the trader's one-week portfolio VaR to not exceed $100,000 with a 99% degree of confidence. She invest in a three-stock portfolio as described in the below table: [table] i | w_i | σ_(1,i) | σ_(2,i) | σ_(3,i) 1 | 0.3 | 0.04 | | 2 | 0.1 | 0.01 | 0.16 | 3 | 0.6 | 0.02 | 0.04 | 0.36 [/table] Calculate Value at Risk of this portfolio. Use z = 2.326. All the variances and covariances in the table are annualized.[Fill in the blank]单项选择题

A

a. $123,839

B

b. $83,536

C

c. $147,400

D

d. $383,927

E

e. $100,000

登录即可查看完整答案

我们收录了全球超50000道真实原题与详细解析,现在登录,立即获得答案。

类似问题

The implied volatility require the assumption of stable variance estimates over time.[Fill in the blank]

With these data the base rate or prevalence of learning difficulty is equal to:

Suppose there exists some variable whose true population distribution is shown in the diagram below. Because of a wealthy benefactor, Quackers is able to run 5000 experiments; in each of these, he samples independently from the true population distribution and measures the mean of the sample. Suppose Quackers runs 200 people in each experiment. Which of the panels A-E above most accurately captures what you would expect the sampling distribution of the mean to look like?

Gladstone Corporation has a plant that can generate a cash flow of $3 million annually. Due to the change of the business environment, the cash flow next year will either increase by 20% or decrease by 20%, with probabilities of 30% and 70%, respectively. Gladstone’s CEO expects the above change to be permanent. The expense to run this plant is $2.5 million per year. The cost of capital for this plant is estimated to be 8% per annum. Gladstone can shut down the plant at a cost of $0.5 million at any time. The value of the option to abandon the plant will be closest to:[Fill in the blank]

更多留学生实用工具

希望你的学习变得更简单

加入我们,立即解锁 海量真题 与 独家解析,让复习快人一步!