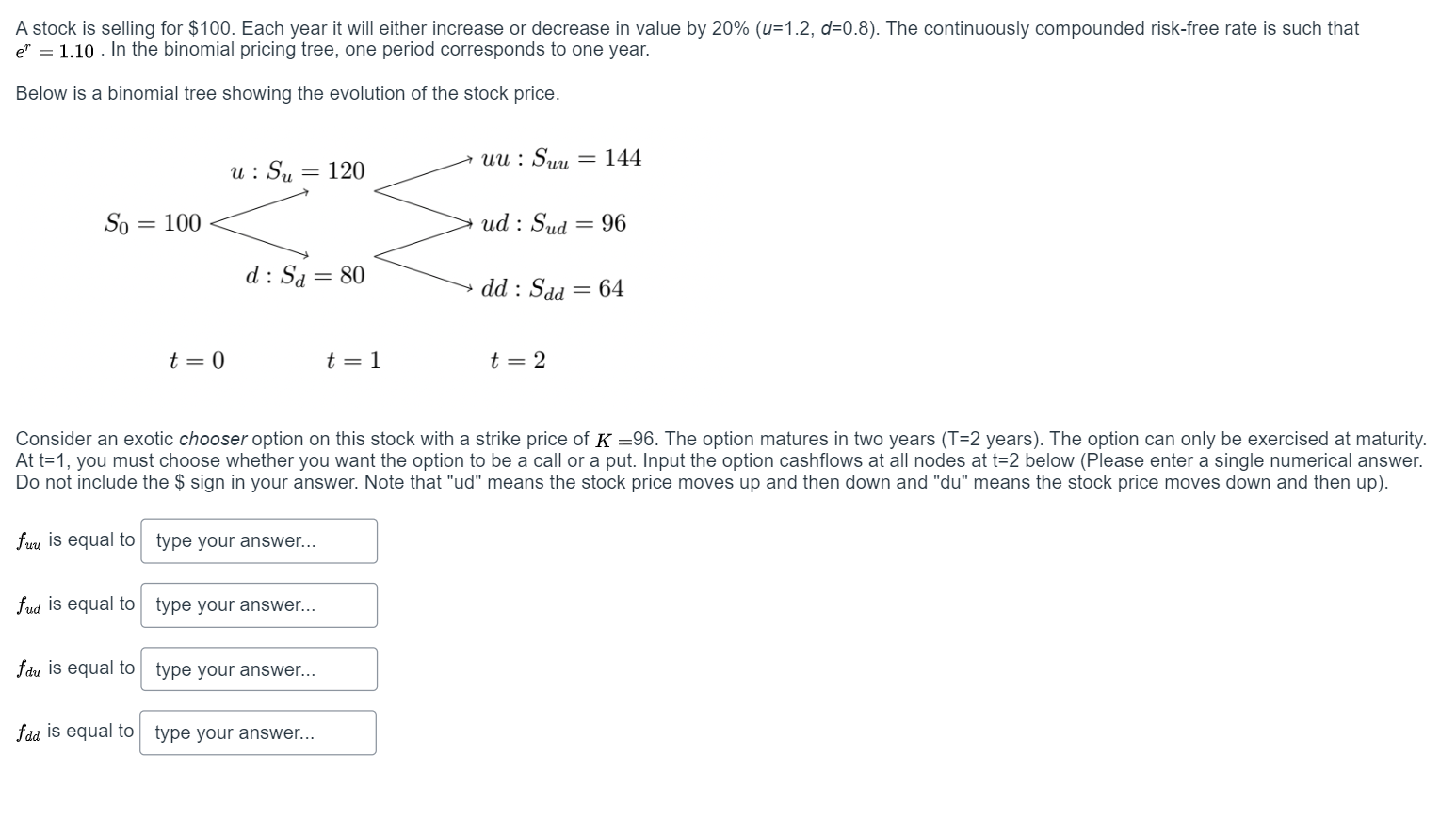

Question at position 8 A stock is selling for $100. Each year it will either increase or decrease in value by 20% (u=1.2, d=0.8). The continuously compounded risk-free rate is such that . In the binomial pricing tree, one period corresponds to one year. Below is a binomial tree showing the evolution of the stock price. Consider an exotic chooser option on this stock with a strike price of 96. The option matures in two years (T=2 years). The option can only be exercised at maturity. At t=1, you must choose whether you want the option to be a call or a put. Input the option cashflows at all nodes at t=2 below (Please enter a single numerical answer. Do not include the $ sign in your answer. Note that "ud" means the stock price moves up and then down and "du" means the stock price moves down and then up). is equal to Question Blank 1 of 4[input] is equal to Question Blank 2 of 4[input] is equal to Question Blank 3 of 4[input] is equal to Question Blank 4 of 4[input]多项填空题

登录即可查看完整答案

我们收录了全球超50000道真实原题与详细解析,现在登录,立即获得答案。

类似问题

Question text 2Marks Call options and put options are written on Qantas.If the interest rate increases, how are the prices of Qantas options affected?Qantas call options will Answer 4[select: , increase, decrease] while Qantas put options will Answer 5[select: , decrease, increase]. Notes Report question issue Question 10 Notes

When the non-dividend paying stock price is $40, the strike price is $42, the risk-free rate is 3% p.a. (continuously compounded), the volatility is 25% and the time to maturity is 6 months, which of the following is the price of a European call option on the stock?[Fill in the blank]

Question text 2Marks A European call option has 8 months to expiry and a strike price of $32.The underlying stock has a current price of $30 and volatility (σ) of 0.50 per annum.The riskfree rate of interest is 5% per annum continuously compounded. Calculate N(d1) as required for the Black-Scholes model Answer 1[input] Enter your answer to 4 decimal places.Notes Report question issue Question 7 Notes

What is the upper bound of an American put option with 7 months to expiry and a strike price of $ 6. The underlying stock is currently trading at $ 1.5, and the risk-free rate is 2.6%. Do not enter the dollar sign "$".

更多留学生实用工具

希望你的学习变得更简单

加入我们,立即解锁 海量真题 与 独家解析,让复习快人一步!