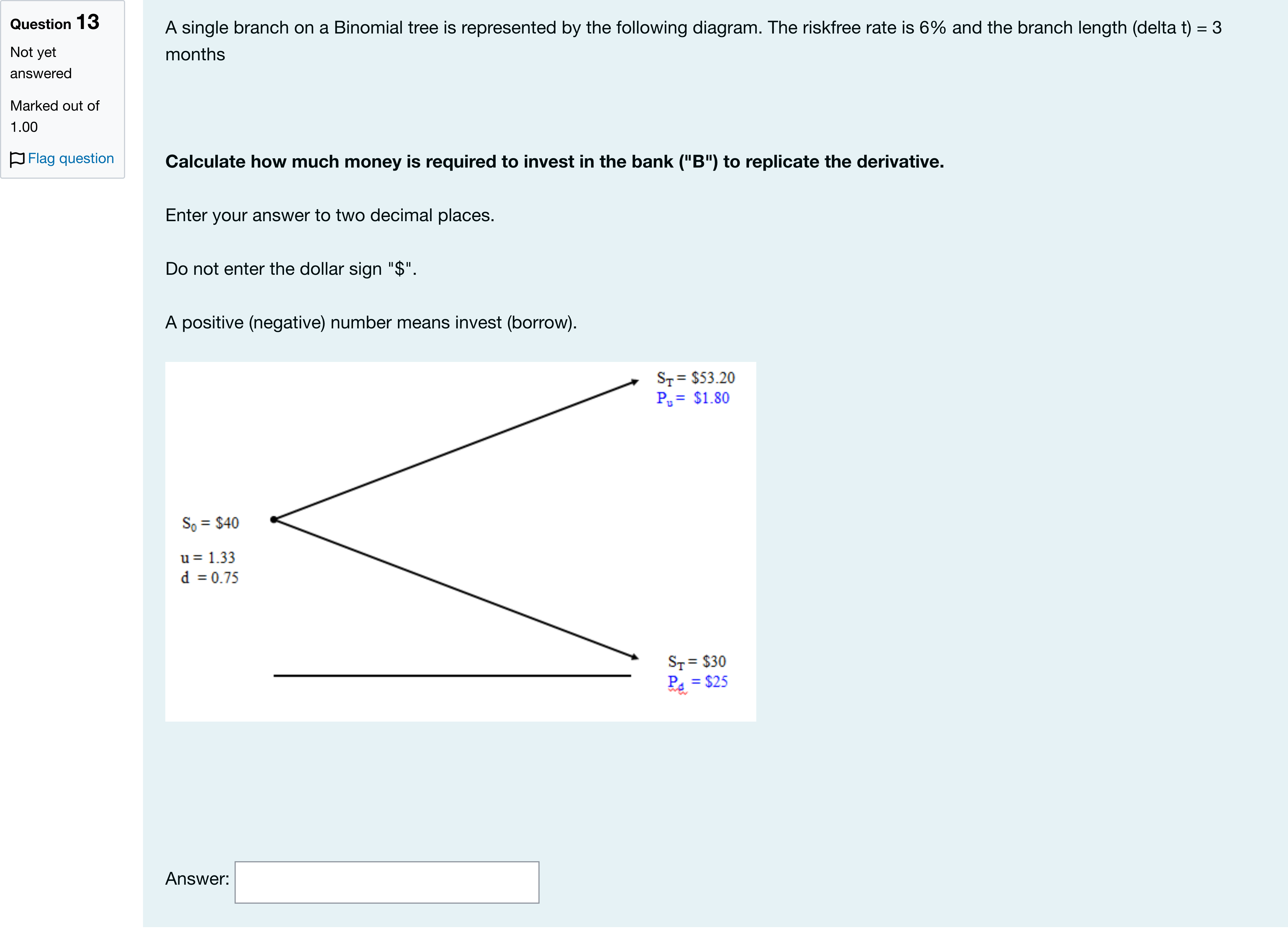

A single branch on a Binomial tree is represented by the following diagram. The riskfree rate is 6% and the branch length (delta t) = 3 months Calculate how much money is required to invest in the bank ("B") to replicate the derivative. Enter your answer to two decimal places. Do not enter the dollar sign "$". A positive (negative) number means invest (borrow).数值题

登录即可查看完整答案

我们收录了全球超50000道真实原题与详细解析,现在登录,立即获得答案。

类似问题

Question text 4Marks An American put option has a strike price of $95 and expires 12 months from now.The following diagram shows a 2-step Binomial tree modelling share-price movements over the 12-month life of this put option. Key details are:the proportional up (u) and down (d) movements on each branch are u = 1.1934 and d = 0.8380 the branch length (δt) is 0.50 the riskfree interest rate is 6% pa continuously compounded. On the upper-right branch labelled with a big number 1, the value of the put option is Answer 2[input]On the lower-right branch labelled with a big number 2, the value of the put option is Answer 3[input].Do not enter a dollar sign in your answer. Enter answers to 2 decimal places.Notes Report question issue Question 19 Notes

Question text 2Marks You are pricing a derivative using the risk-neutral approach on a Binomial tree.The length of each branch in the tree (δt) is 3 months.The riskfree interest rate is 4% per annum continuously compounded.The proportional up movement in stock price is u = 1.2214.Calculate the risk-neutral probability (p*) that share price will move up Answer 1[input]Enter your answer to 4 decimal places. For example, if the probabiliy is 52.34%, enter 0.5234.Notes Report question issue Question 17 Notes

Question text 5Marks The following diagram depicts the valuation of a European put option which has a strike price of $55 using a 1-step Binomial tree.The proportional up (u) and down (d) movements on this tree are 1.2840 and 0.7788 respectively.The branch length (δt) is 0.25 .The riskfree interest rate (r) is 6% continuously compounded.You will calculate the value of this put option today (P0) using the delta-hedging approach.Answer each of the following questions, giving your answer to 2 decimal places.If the calculated number is negative, be sure to enter the negative sign in the box.Do not enter the dollar sign ($).On this branch, delta (Δ) is equal to Answer 6[input] which means that you need to Answer 7[select: , short sell, long] the underlying shares.At time 0, in addition to entering a position of Δ shares, you also need to enter a Answer 8[select: , short, long] position in the put option itself.If you set up a delta hedge at time 0, the dollar value of your 2-piece delta-hedged portfolio at the end of the branch is Answer 9[input]At time 0, the value of the put option (P0) is Answer 10[input]Notes Report question issue Question 15 Notes

Question text 5Marks The following diagram depicts the valuation of a European call option which has a strike price of $50 using a 1-step Binomial tree.The proportional up (u) and down (d) movements on this tree are 1.1912 and 0.8395 respectively.The branch length (δt) is 0.25 .The riskfree interest rate (r) is 7% continuously compounded.You will calculate the value of this call option today (C0) using the replication approach.Answer each of the following questions, giving your answer to 2 decimal places.if the calculated number is negative, be sure to enter the negative sign in the box.Do not enter the dollar sign ($).On this branch, delta (Δ) is equal to Answer 1[input] which means that you need to Answer 2[select: , long, short] the underlying shares.On this branch, "B" is equal to Answer 3[input] which means that you need to Answer 4[select: , borrow, invest] this amount at the bank.At time 0, the value of the call option (C0) is Answer 5[input]Notes Report question issue Question 14 Notes

更多留学生实用工具

希望你的学习变得更简单

加入我们,立即解锁 海量真题 与 独家解析,让复习快人一步!