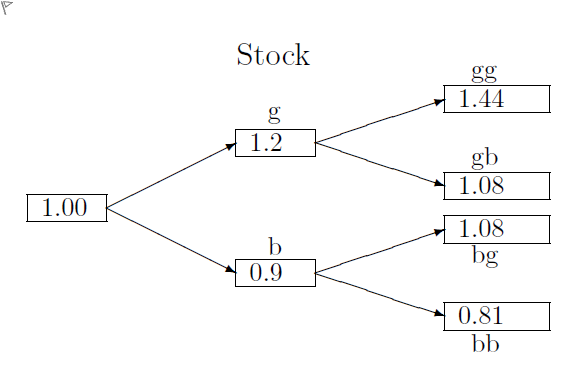

Question textThe following information refers to parts A-B below, select the right answer from the drop-down menu. Consider a three period binomial time-state model in which there are two securities, a bond and a stock. The bond price increases [math: 2%]2\% of its prior value in every period and its initial price is 1. The payments made by the stock are shown in the binomial tree below: The [math: Patom]\mathbf {P_{atom}} vector represents the atomic (time-state) prices of elementary payment for states [math: g], [math: b], [math: gg], [math: gb], [math: bg] and [math: bb], respectively, rounded to 4 decimal digits. [math: Patom=(0.3922,0.5882,0.1538,0.2307,0.2307,?)] \mathbf {P_{atom}}=(0.3922, 0.5882, 0.1538, 0.2307, 0.2307, ?) A) The discount factor of period 1 is: Answer 1 Question 5[select: , 0.30, 0.83, 0.98, 1.94, none of the above] B) The atomic security price of state [math: bb] is equal to: Answer 2 Question 5[select: , 0.1560, 0.2360, 0.2560, 0.3460, 0.4060]多项填空题

登录即可查看完整答案

我们收录了全球超50000道真实原题与详细解析,现在登录,立即获得答案。

类似问题

For some value of p, the payoff associated with node F is 4045.16, and the payoff associated with G is -842.99. What is the payoff associated with node C?

Question textThe following information refers to parts A-B below, select the right answer from the drop-down menu. Consider a three period binomial time-state model in which there are two securities, a bond and a stock. The bond price increases [math: 2%]2\% of its prior value in every period and its initial price is 1. The payments made by the stock are shown in the binomial tree below: The [math: Patom]\mathbf {P_{atom}} vector represents the atomic (time-state) prices of elementary payment for states [math: g], [math: b], [math: gg], [math: gb], [math: bg] and [math: bb], respectively, rounded to 4 decimal digits. [math: Patom=(0.3922,0.5882,0.1538,0.2307,0.2307,?)] \mathbf {P_{atom}}=(0.3922, 0.5882, 0.1538, 0.2307, 0.2307, ?) A) The discount factor of period 1 is: Answer 1 Question 7[select: , 0.30, 0.83, 0.98, 1.94, none of the above] B) The atomic security price of state [math: bb] is equal to: Answer 2 Question 7[select: , 0.1560, 0.2360, 0.2560, 0.3460, 0.4060]

Question textThe following information refers to parts A-B below, select the right answer from the drop-down menu. Consider a three period binomial time-state model in which there are two securities, a bond and a stock. The bond price increases [math: 2%]2\% of its prior value in every period and its initial price is 1. The payments made by the stock are shown in the binomial tree below: The [math: Patom]\mathbf {P_{atom}} vector represents the atomic (time-state) prices of elementary payment for states [math: g], [math: b], [math: gg], [math: gb], [math: bg] and [math: bb], respectively, rounded to 4 decimal digits. [math: Patom=(0.3922,0.5882,0.1538,0.2307,0.2307,?)] \mathbf {P_{atom}}=(0.3922, 0.5882, 0.1538, 0.2307, 0.2307, ?) A) The discount factor of period 1 is: Answer 1 Question 3[select: , 0.30, 0.83, 0.98, 1.94, none of the above] B) The atomic security price of state [math: bb] is equal to: Answer 2 Question 3[select: , 0.1560, 0.2360, 0.2560, 0.3460, 0.4060]

You are operating a gas turbine power station (GTPS). The risk factor driving cash inflows (revenues) is the electricity price. The risk factor driving cash outflows (expenses) is the gas price. At current prices, the yearly gas bill is EUR 50m (assume payment upfront) for producing a volume of electric power that can be sold for EUR 55m on the market (assume payment upfront).The electricity and gas price follow a multiplicative binomial distribution with the parameters u=1.8 and d =0.6 (electricity) and u=1.5 and d=0.8 (gas). Also for simplicity, we assume perfect correlation. The objective probability q for an upward movement is 0.5. The risk-free rate is equal 8.00% per yearWhat is the value of the GTPS closest to, if it lives for two years and one binomial step is equal one year? Conduct the valuation on a risk-neutral basis.

更多留学生实用工具

希望你的学习变得更简单

加入我们,立即解锁 海量真题 与 独家解析,让复习快人一步!