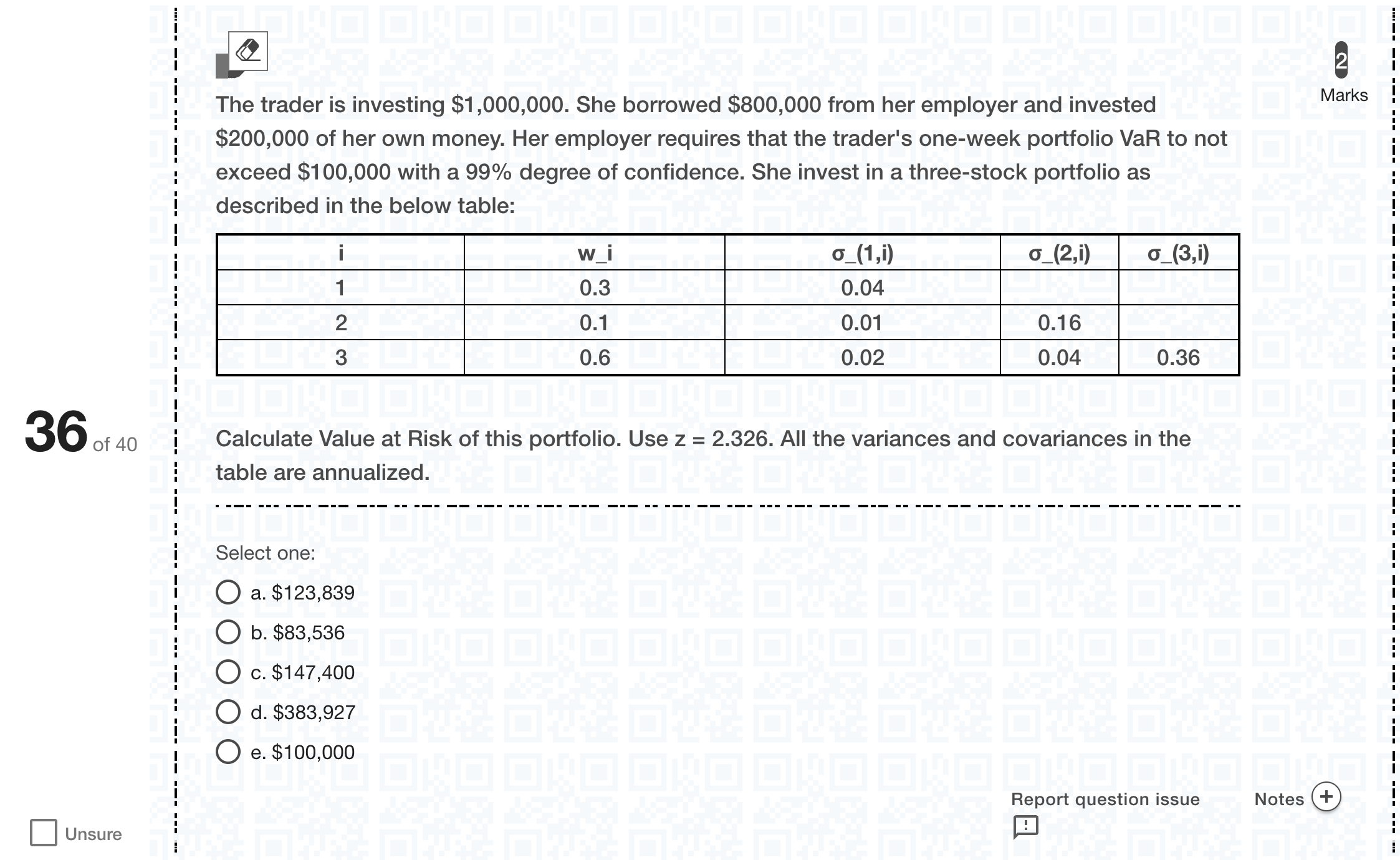

The trader is investing $1,000,000. She borrowed $800,000 from her employer and invested $200,000 of her own money. Her employer requires that the trader's one-week portfolio VaR to not exceed $100,000 with a 99% degree of confidence. She invest in a three-stock portfolio as described in the below table: [table] i | w_i | σ_(1,i) | σ_(2,i) | σ_(3,i) 1 | 0.3 | 0.04 | | 2 | 0.1 | 0.01 | 0.16 | 3 | 0.6 | 0.02 | 0.04 | 0.36 [/table] Calculate Value at Risk of this portfolio. Use z = 2.326. All the variances and covariances in the table are annualized.[Fill in the blank]Single choice

A

a. $123,839

B

b. $83,536

C

c. $147,400

D

d. $383,927

E

e. $100,000

Log in for full answers

We've collected over 50,000 authentic original questions and detailed explanations from around the globe. Log in now and get instant access to the answers!

Similar Questions

The implied volatility require the assumption of stable variance estimates over time.[Fill in the blank]

With these data the base rate or prevalence of learning difficulty is equal to:

Suppose there exists some variable whose true population distribution is shown in the diagram below. Because of a wealthy benefactor, Quackers is able to run 5000 experiments; in each of these, he samples independently from the true population distribution and measures the mean of the sample. Suppose Quackers runs 200 people in each experiment. Which of the panels A-E above most accurately captures what you would expect the sampling distribution of the mean to look like?

Gladstone Corporation has a plant that can generate a cash flow of $3 million annually. Due to the change of the business environment, the cash flow next year will either increase by 20% or decrease by 20%, with probabilities of 30% and 70%, respectively. Gladstone’s CEO expects the above change to be permanent. The expense to run this plant is $2.5 million per year. The cost of capital for this plant is estimated to be 8% per annum. Gladstone can shut down the plant at a cost of $0.5 million at any time. The value of the option to abandon the plant will be closest to:[Fill in the blank]

More Practical Tools for Students Powered by AI Study Helper

Making Your Study Simpler

Join us and instantly unlock extensive past papers & exclusive solutions to get a head start on your studies!