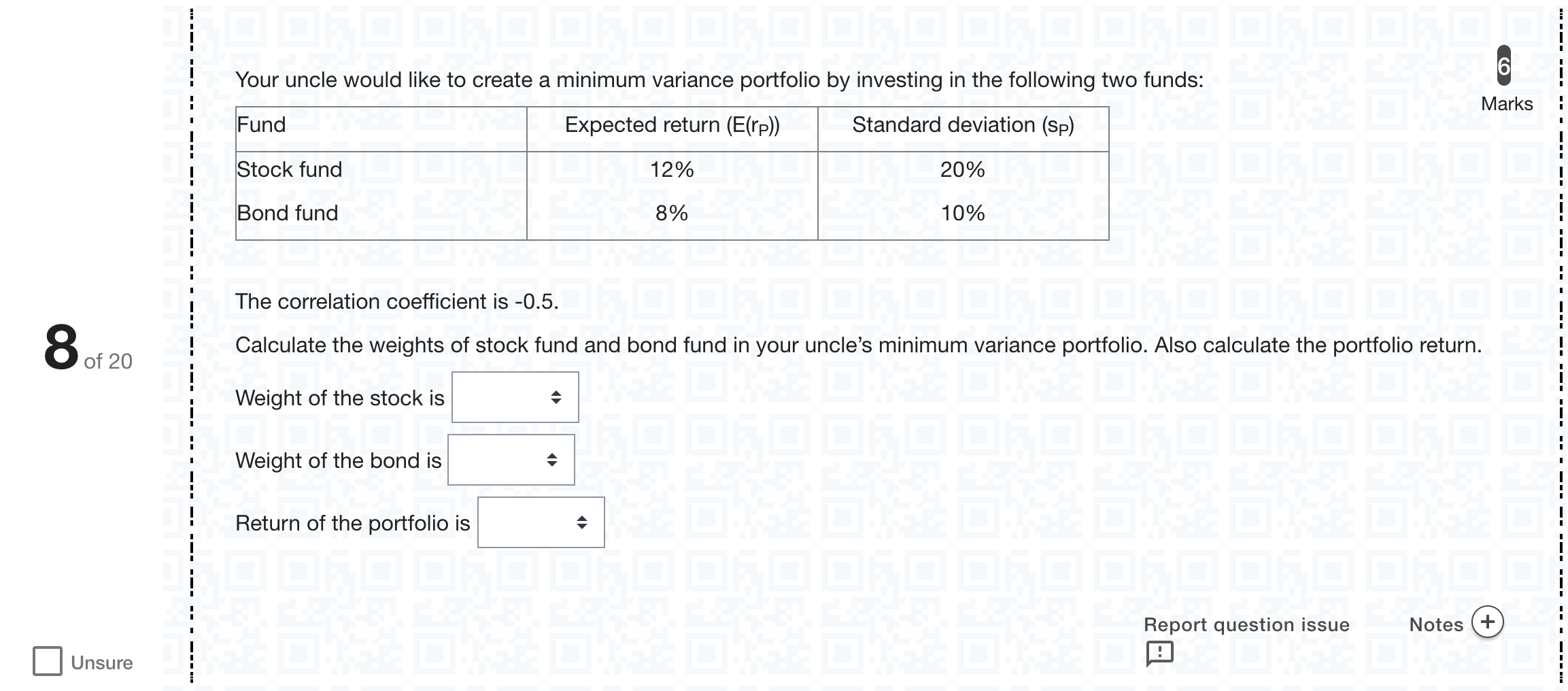

Question text 6Marks Your uncle would like to create a minimum variance portfolio by investing in the following two funds: [table] Fund | Expected return (E(rP)) | Standard deviation (sP) Stock fund Bond fund | 12% 8% | 20% 10% [/table] The correlation coefficient is -0.5. Calculate the weights of stock fund and bond fund in your uncle’s minimum variance portfolio. Also calculate the portfolio return. Weight of the stock is Answer 9[select: , 28.57%, 51.22%, 67.25%, 59.71%, 65.01%] Weight of the bond is Answer 10[select: , 71.42%, 48.78%, 32.75%, 40.29%, 34.09%] Return of the portfolio is Answer 11[select: , 10.71%, 9.11%, 11.29%, 9.87%, 10.08%]Notes Report question issue Question 8 NotesMultiple fill-in-the-blank

Log in for full answers

We've collected over 50,000 authentic original questions and detailed explanations from around the globe. Log in now and get instant access to the answers!

Similar Questions

You invest $1,500 in a risky asset with an expected rate of return of 0.30 and a standard deviation of 0.55 and a T-bill with a rate of return of 0.05. What percentages of your money must be invested in the risky asset and the risk-free asset, respectively, to form a portfolio with an expected return of 0.25?[Fill in the blank]

Question1.3 An investor’s optimal risky allocation y* is required to identify the______: Optimal Complete Portfolio C*. Global Minimum Variance Portfolio (GMVP). Optimal risky portfolio P*. Capital Allocation Line (CAL). Efficient frontier. ResetMaximum marks: 2.5 Flag question undefined

Constraining MSR portfolio weights to the (0%, 100%) range compared to allowing unconstrained (short-selling) weights tends to:

The Global Minimum Variance (GMV) portfolio is defined as the portfolio that:

More Practical Tools for Students Powered by AI Study Helper

Making Your Study Simpler

Join us and instantly unlock extensive past papers & exclusive solutions to get a head start on your studies!