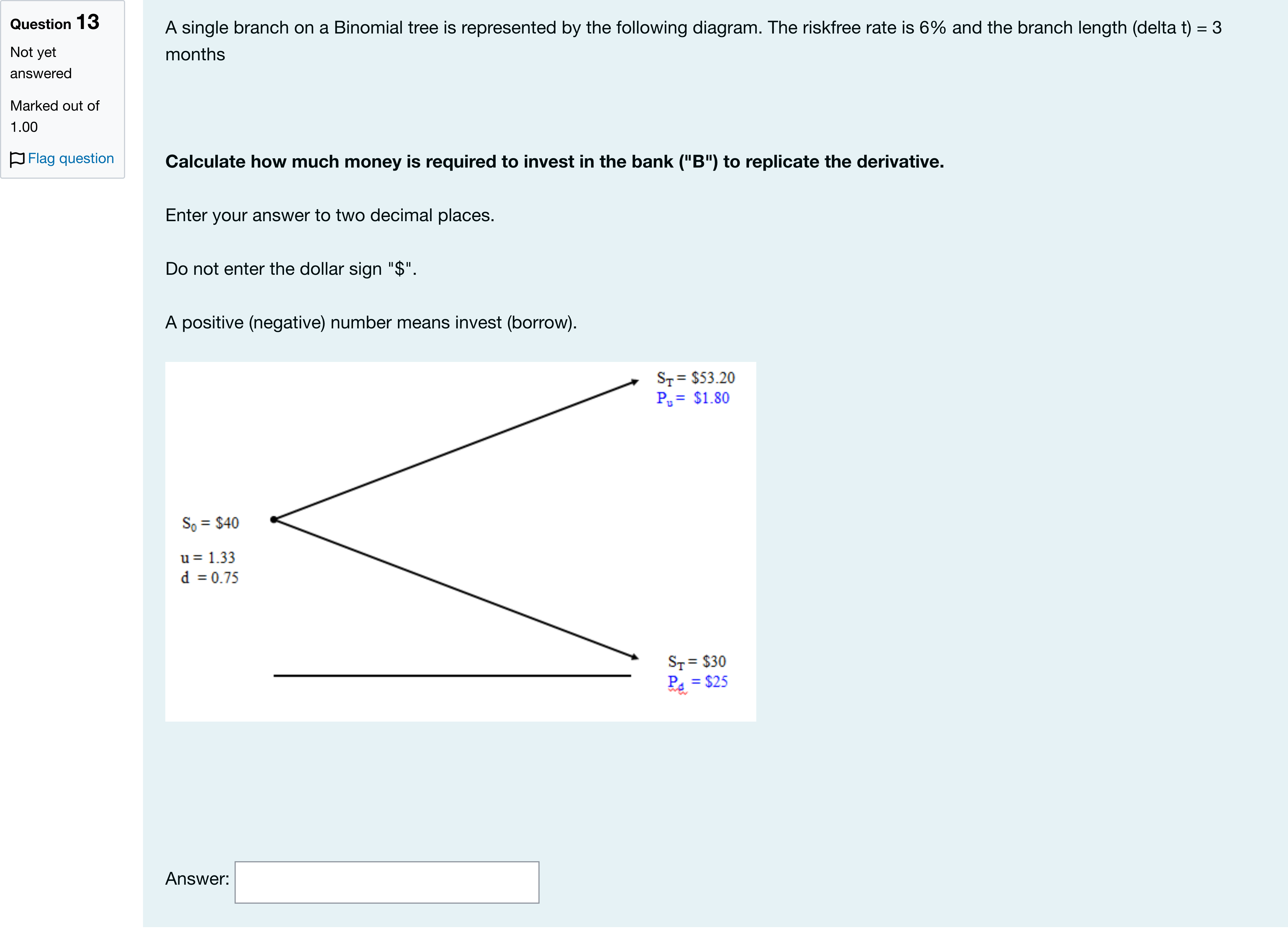

A single branch on a Binomial tree is represented by the following diagram. The riskfree rate is 6% and the branch length (delta t) = 3 months Calculate how much money is required to invest in the bank ("B") to replicate the derivative. Enter your answer to two decimal places. Do not enter the dollar sign "$". A positive (negative) number means invest (borrow).Numerical

Log in for full answers

We've collected over 50,000 authentic original questions and detailed explanations from around the globe. Log in now and get instant access to the answers!

Similar Questions

Question text 4Marks An American put option has a strike price of $95 and expires 12 months from now.The following diagram shows a 2-step Binomial tree modelling share-price movements over the 12-month life of this put option. Key details are:the proportional up (u) and down (d) movements on each branch are u = 1.1934 and d = 0.8380 the branch length (δt) is 0.50 the riskfree interest rate is 6% pa continuously compounded. On the upper-right branch labelled with a big number 1, the value of the put option is Answer 2[input]On the lower-right branch labelled with a big number 2, the value of the put option is Answer 3[input].Do not enter a dollar sign in your answer. Enter answers to 2 decimal places.Notes Report question issue Question 19 Notes

Question text 2Marks You are pricing a derivative using the risk-neutral approach on a Binomial tree.The length of each branch in the tree (δt) is 3 months.The riskfree interest rate is 4% per annum continuously compounded.The proportional up movement in stock price is u = 1.2214.Calculate the risk-neutral probability (p*) that share price will move up Answer 1[input]Enter your answer to 4 decimal places. For example, if the probabiliy is 52.34%, enter 0.5234.Notes Report question issue Question 17 Notes

Question text 5Marks The following diagram depicts the valuation of a European put option which has a strike price of $55 using a 1-step Binomial tree.The proportional up (u) and down (d) movements on this tree are 1.2840 and 0.7788 respectively.The branch length (δt) is 0.25 .The riskfree interest rate (r) is 6% continuously compounded.You will calculate the value of this put option today (P0) using the delta-hedging approach.Answer each of the following questions, giving your answer to 2 decimal places.If the calculated number is negative, be sure to enter the negative sign in the box.Do not enter the dollar sign ($).On this branch, delta (Δ) is equal to Answer 6[input] which means that you need to Answer 7[select: , short sell, long] the underlying shares.At time 0, in addition to entering a position of Δ shares, you also need to enter a Answer 8[select: , short, long] position in the put option itself.If you set up a delta hedge at time 0, the dollar value of your 2-piece delta-hedged portfolio at the end of the branch is Answer 9[input]At time 0, the value of the put option (P0) is Answer 10[input]Notes Report question issue Question 15 Notes

Question text 5Marks The following diagram depicts the valuation of a European call option which has a strike price of $50 using a 1-step Binomial tree.The proportional up (u) and down (d) movements on this tree are 1.1912 and 0.8395 respectively.The branch length (δt) is 0.25 .The riskfree interest rate (r) is 7% continuously compounded.You will calculate the value of this call option today (C0) using the replication approach.Answer each of the following questions, giving your answer to 2 decimal places.if the calculated number is negative, be sure to enter the negative sign in the box.Do not enter the dollar sign ($).On this branch, delta (Δ) is equal to Answer 1[input] which means that you need to Answer 2[select: , long, short] the underlying shares.On this branch, "B" is equal to Answer 3[input] which means that you need to Answer 4[select: , borrow, invest] this amount at the bank.At time 0, the value of the call option (C0) is Answer 5[input]Notes Report question issue Question 14 Notes

More Practical Tools for Students Powered by AI Study Helper

Making Your Study Simpler

Join us and instantly unlock extensive past papers & exclusive solutions to get a head start on your studies!